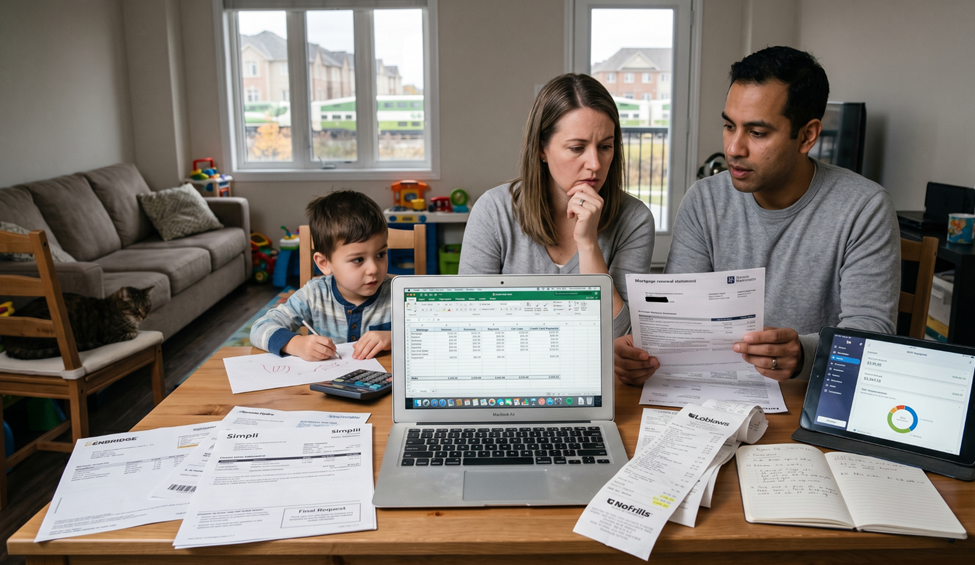

Financial stability remains a significant challenge for many Canadian families and individuals. Rising living costs, high interest rates, and unexpected expenses continue to push households toward debt. According to recent Statistics Canada data, consumer debt levels remain elevated across the country, with Ontario residents carrying some of the highest burdens. In Toronto and the Greater Toronto Area, where the cost of living is among the highest in Canada, many people find themselves juggling multiple debts while trying to maintain day to day financial security. Average household debt in Ontario exceeds $200,000 when including mortgages, and non-mortgage debt such as credit cards, lines of credit, and personal loans continues to create heavy pressure for thousands of families.

Effective debt relief strategies often focus on budgeting, negotiation with creditors, consumer proposals, and long term financial counseling. However, one powerful but frequently overlooked tool in the journey toward financial freedom is strategic tax planning. When managed correctly, tax optimization can free up substantial cash flow, reduce liabilities, and create breathing room for faster debt repayment and stronger financial recovery.

Successful financial recovery requires a comprehensive approach that addresses both immediate debt pressures and underlying financial systems. Many individuals and families working with debt relief and financial counseling services discover that aligning their tax situation with their broader recovery goals delivers meaningful and sometimes life changing results.

Working with the Premier tax accountant in Toronto has helped numerous clients identify legitimate ways to minimize tax burdens, claim overlooked credits and deductions, and structure their finances to support sustainable debt reduction and long term stability.

The Connection Between Tax Planning and Debt Relief

Tax obligations can significantly impact cash flow for those carrying debt. For individuals and families in repayment programs or negotiating settlements, every dollar saved on taxes becomes available for debt reduction or building emergency savings. In 2026, with inflation adjusted brackets, updated Canada Pension Plan contributions, and evolving CRA rules, proactive tax planning has become an essential component of effective financial counseling.

Many people in debt situations are surprised to learn they may be eligible for additional credits and benefits. The Canada Workers Benefit, GST HST credit, Ontario Trillium Benefit, Ontario Energy and Property Tax Credit, and various provincial supports can provide crucial extra funds when claimed properly. For self employed individuals or those with side income, understanding business expense deductions, home office claims, vehicle expense tracking, and capital cost allowance can create substantial savings that directly support debt repayment plans. Expense management software comes in handy here, allowing you the mental space and time to think critically outside of manual expense tracking.

Strategic tax planning also helps prevent new tax debts from accumulating. By staying current with filings, making appropriate installment payments, and addressing any past issues through the Voluntary Disclosure Program, individuals protect their recovery progress from CRA collections actions that could derail debt relief efforts. Late filed returns or unpaid tax balances can lead to aggressive collection measures including wage garnishments and bank account freezes, which complicate existing debt management agreements.

Key Tax Strategies That Support Financial Recovery

Effective tax planning for those in debt relief involves several practical areas. First, maximizing refundable credits is essential. Many low and moderate income households qualify for significant refunds through programs designed to support financial stability. Proper filing ensures these credits are received promptly and can be applied toward high interest credit card debt or consolidated loans.

For homeowners facing mortgage stress, understanding the tax implications of potential debt consolidation, consumer proposals, or bankruptcy remains important. While certain debt relief options have specific tax consequences, strategic planning can help minimize unexpected tax bills during the recovery process. For example, forgiven debt under a consumer proposal may have tax implications in some cases, but proper timing and professional advice can often reduce or manage these liabilities effectively.

Self employed individuals and small business owners in Toronto often benefit from reviewing capital cost allowance claims, inventory valuation methods, and legitimate business expense tracking. These deductions can lower taxable income and improve cash flow during challenging periods. Additionally, contributing to Registered Retirement Savings Plans or Tax Free Savings Accounts within allowable limits can provide both tax advantages and long term financial security, even while actively working on debt reduction.

Other valuable strategies include medical expense credits for those dealing with health related financial stress, childcare expense deductions for working parents, and tuition credits for individuals pursuing education to improve earning potential. Each of these can generate additional refunds or reduced tax payable that accelerates debt payoff timelines.

Common Tax Related Challenges During Debt Recovery

Individuals navigating debt relief frequently encounter tax related obstacles. Unfiled or late tax returns can trigger CRA enforcement actions, including wage garnishments that conflict with debt repayment agreements. Outstanding tax debts may also reduce eligibility for certain government benefits or complicate consumer proposal negotiations with creditors.

Poor record keeping makes it difficult to claim legitimate deductions, resulting in higher than necessary tax payments. For those with irregular income from gig work, consulting, ride sharing, or seasonal employment, accurate tracking of expenses becomes even more critical for both tax compliance and overall financial management.

The Voluntary Disclosure Program offers a pathway to address past tax issues with reduced penalties and interest, but timing and proper documentation are essential. Working with experienced professionals helps individuals correct compliance problems while protecting their broader debt relief objectives. Many clients have successfully used this program to clean up old returns without facing full penalties, allowing them to focus fully on debt reduction.

Another common challenge involves balancing tax installment payments with debt repayment priorities. Professional guidance can help create a realistic payment schedule that satisfies the CRA while maintaining momentum on consumer debts.

Building a Sustainable Financial Future Through Integrated Planning

True financial recovery extends beyond simply reducing current debt. It involves creating systems that prevent future financial distress. Strategic tax planning plays a central role by improving cash flow management, encouraging saving habits, and supporting informed financial decisions.

Many clients who combine debt relief counseling with proactive tax strategies report faster progress toward financial freedom. They learn to view tax filing not as an annual burden but as an opportunity to strengthen their overall financial position. This integrated approach often leads to improved credit scores, greater peace of mind, and a clearer path toward long term goals such as home ownership, retirement planning, business development, or children’s education savings.

In Toronto’s high cost environment, where housing expenses, transportation costs, TTC fares, and everyday living expenses place significant pressure on budgets, optimizing every available dollar through legitimate tax planning becomes particularly valuable for families working toward debt freedom. Small consistent savings from tax optimization can compound over time and create meaningful momentum.

Practical Steps to Combine Tax Planning with Debt Relief

Start by gathering all relevant financial documents including previous tax returns, notices of assessment, pay stubs, and expense records. Review your current tax situation with a qualified professional who understands both taxation and debt recovery. Identify any unfiled returns, outstanding balances, or missed credits that could impact your debt recovery plan. Similar to how digital solutions have streamlined the process of lodging an online tax return Australia, modern tax preparation tools and professional services can help individuals stay compliant, access eligible credits, and reduce the risk of costly filing errors that may affect broader financial recovery goals.

Develop a realistic timeline for addressing tax obligations while maintaining momentum on debt repayment. Consider meeting regularly with both a financial counselor and a tax professional who understand the intersection of debt relief and taxation. This collaborative approach ensures all strategies work together rather than creating conflicts between different financial goals.

Maintain detailed records throughout the year. Whether tracking mileage for work related travel, home office expenses, medical costs, or charitable donations, good documentation supports stronger tax positions and provides valuable insights for budgeting and financial planning. Many free or low cost apps and tools can help simplify this process for busy individuals.

Looking Ahead: Tax Planning as Part of Long Term Financial Wellness

As we move further into 2026 and beyond, tax rules will continue evolving alongside economic conditions. Staying informed and working with knowledgeable professionals helps individuals and families adapt their strategies while maintaining progress toward debt freedom and financial security.

Toronto residents facing debt challenges have access to a strong network of financial counseling, legal assistance, and tax professionals who can provide coordinated support. By taking a holistic approach that addresses immediate debt relief needs while building stronger financial habits, many people successfully achieve lasting stability and renewed hope for the future.

The journey toward financial freedom is rarely straightforward, but with the right combination of debt relief strategies, financial counseling, and strategic tax planning, sustainable recovery becomes achievable for more Canadians. Taking control of your tax situation is often one of the most empowering steps you can take on the path to financial wellness.

Frequently Asked Questions

Can tax refunds be used toward debt repayment?

Yes. Many debt relief programs allow or even encourage the use of tax refunds to accelerate repayment. A qualified tax professional can help maximize eligible refunds while ensuring compliance with any existing agreements.

Does filing for consumer proposals or bankruptcy affect my taxes?

It can. Certain debt relief options have specific tax implications. Professional guidance helps minimize unexpected tax consequences and ensures proper reporting during and after the process.

How can someone in debt improve their tax situation?

Start by filing all outstanding returns, claiming all eligible credits and deductions, and setting up a payment plan if tax debts exist. Strategic planning with an experienced advisor often uncovers additional savings that support debt reduction.

Is it worth consulting a tax professional while in a debt relief program?

Absolutely. A knowledgeable tax advisor can identify opportunities to reduce current and future tax burdens, protect benefits, and ensure tax strategies align with your overall debt relief and financial recovery goals.

What should I do if I have both tax debt and consumer debt?

Prioritize based on collection risk and interest rates. The CRA has strong collection powers, so addressing tax debt strategically while continuing debt relief negotiations is often recommended. Professional advice helps create a balanced plan.